ARTICLE

Major Gifts 101: What You Need to Know to Raise More

Major donors normally contribute the majority of nonprofits’ annual revenue. When you have so few donors contributing the lion’s share of your donations, it can put your mission in jeopardy should you lose even one of those major donors.

Because major gifts are so large, cultivating and acquiring more of these donations requires time and dedication. In this guide, we’ll cover the need-to-know information and steps to create a major gift fundraising strategy, including:

Let’s start by reviewing the basics of these key donations.

Major gifts are the largest donations your nonprofit receives. These donations are key drivers of major fundraising efforts and give your nonprofit the foundation to successfully pursue major projects and expand its mission.

For example, major gifts make up the bulk of funding for significant campaigns like capital or comprehensive campaigns, enabling your nonprofit to access the funds it needs to build new facilities, launch new programs, or purchase necessary equipment.

The exact donation amount you consider a major gift will depend on the highest donation amounts your organization typically receives. For example, if your largest donations are between $25,000 and $50,000, you might designate that as your major gift range.

Some larger organizations may consider major donations to be $100,000 or more, while smaller nonprofits might consider $1,000 donations to be major gifts.

Major gifts make up the bulk of a nonprofit’s annual fund. They allow your nonprofit to remain in operation and tackle major undertakings, such as implementing renovations or establishing new programs.

Creating a major gift program or fundraising strategy is essential because major gifts do not just appear out of thin air. They require careful planning, cultivation, and stewardship to acquire them and turn major donors into recurring supporters.

According to Giving USA 2024, very large “mega-gifts” totaled $8.07 billion in 2023. A major gift fundraising strategy helps ensure that more of these massive donations are coming your nonprofit’s way.

Major donors are the individuals who contribute major gifts to your nonprofit. These supporters can come from all walks of life, but most share specific characteristics that make it easier to identify them. Understanding who major donors are can help you find more of these individuals within your nonprofit’s CRM and start building relationships with them.

The following characteristics typically define major donors:

In addition to these traits, major donors are often older. An EverTrue study found that “The average age for first-time major donors has risen from 55 to 66 over the last two decades.” Older adults have greater purchasing power, so it’s often worth directing more of your attention to older prospective donors.

What do major gifts actually look like? These donations come in multiple forms, and your organization should offer more than one type of major giving to appeal to a wider range of donor preferences.

Here are some common types of major gifts:

These gifts are direct donations of cash or checks to your organization. While it’s uncommon for a donor to sit down in your office and make a massive lump sum payment, it can happen occasionally. However, convincing a donor to drop a major gift in one payment is more challenging, and it typically only occurs among your highest net worth, most passionate major donors.

These gift types aren’t major drivers of nonprofit growth, either—a Texas Tech study found that over a five-year period (2010-2015), organizations that received only cash gifts achieved 11% growth, barely keeping pace with inflation.

In contrast to check or cash donations, stock gifts offer greater growth potential for your organization. The Texas study found that organizations that received securities and other non-cash gifts achieved 66% growth in the same five-year period.

Often, donors see stock gifts as less costly for their personal finances because they’re separate from their personal checking or savings accounts. Stock gifts allow them to pull from a different bucket that has less of an impact on their daily lives.

Plus, according to our recent blog post on this topic, gifts of stock can have greater tax benefits than direct cash donations. Stock gifts offer both income tax deductions and avoidance of capital gains taxes on the appreciation. In other words, the donor can deduct the full value of the stock from their taxable income and avoid paying taxes on any increase in the stock value if it goes up.

To accept stock gifts, your nonprofit must set up a brokerage account, spotlight stock gifts on its website’s “ways to give” page, and promote this giving option across marketing channels like email and social media.

Similar to gifts of stock, donations of real estate allow major donors to contribute an asset rather than a direct cash gift to your organization. Donors receive the same tax benefits of avoiding capital gains taxes, while your nonprofit can receive the property’s full value as a tax-exempt organization.

We recommend developing a gift acceptance policy to avoid accepting subpar real estate gifts. In addition, consult with your organization’s legal team to manage the complexities of accepting these donations.

These donations are gifts that donors pledge as part of their will or estate planning. Your organization will collect these gifts when the donor passes away.

When asking for a planned or legacy gift, emphasize the donor’s ability to leave a lasting positive impact on your cause. Provide detailed information about how donors can set up your organization as a beneficiary of a charitable trust or bequest. For example, they may need to speak with a trust attorney or financial advisor to determine the best path forward for their will planning.

Donor-advised funds are personal charitable investment accounts that donors can use to send funding to various charitable organizations. Donors can contribute cash, securities, and other assets to the account and use it as a holding ground until they determine which charities they’d like to support.

Let donors know that your nonprofit accepts DAF donations, and include information about contributing these funds on your website. You can also include details about enabling DAF transfers and even testimonials from DAF donors explaining why this giving option benefited them.

A donor will rarely make a major donation out of the blue. Therefore, one of the best ways to encourage donors to make major gifts is by building relationships with supporters and focusing on donor retention and stewardship.

Let’s review the key steps of finding major donor prospects, building relationships, and retaining their support for the long term:

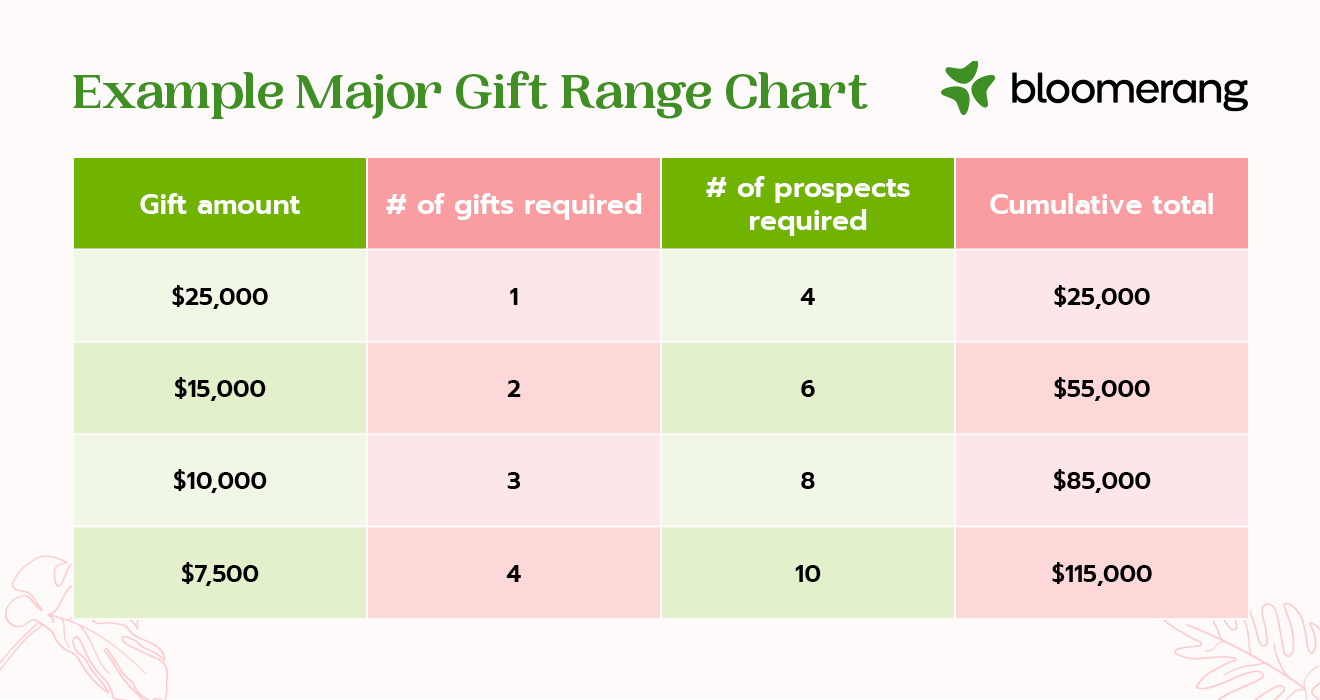

To kick off your major gift fundraising strategy, you should first identify your nonprofit’s unique major gift range. This allows you to understand who your major donors are, what leads them to give at a high level, and how you can build relationships with them and potential major donors to foster a sustainable giving stream.

Follow these steps to outline your organization’s definition of major gifts:

As you set goals for your major giving efforts, be realistic, but optimistic. Understand your nonprofit’s limitations and challenges, but show your team that you believe that they can take your major giving program to new heights.

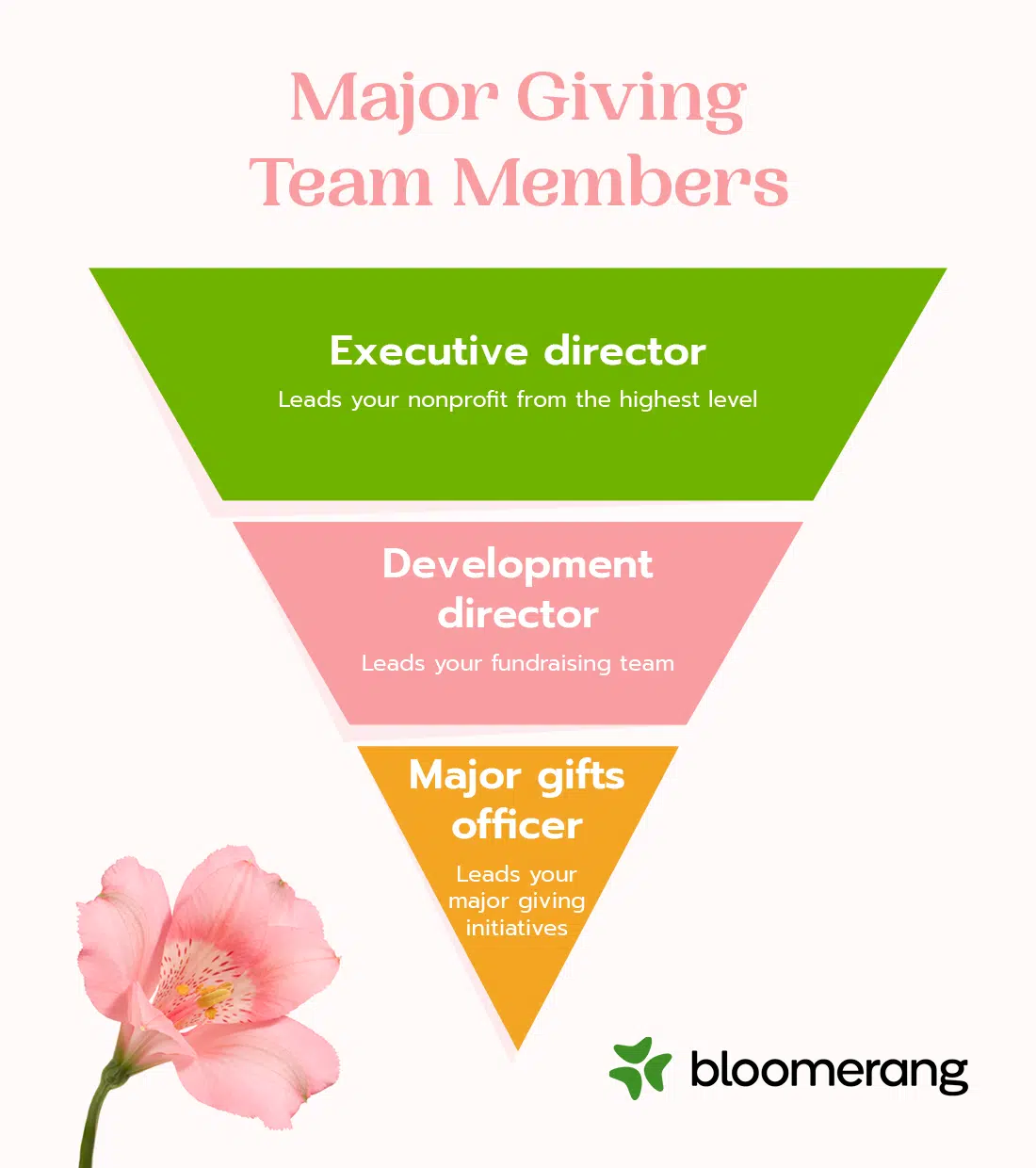

Who will be responsible for acquiring and building relationships with major donors? Assigning responsibilities ensures that everyone is clear on their role in the major giving process.

Your major giving efforts may be supported by these team members:

These core team members may also interact with other staff members to push certain initiatives forward. For example, they may collaborate with your donor recognition team, event planner, volunteer coordinator, and marketing manager.

One of the most common major giving challenges nonprofits face is trying to engage with lukewarm or cold prospects. That’s why it’s important to approach the right donors at the right time. Here’s how to identify the best major gift prospects for your organization.

Generally, donors with a history of giving, high engagement with your organization, and a high generosity score (capacity for donating) will be the best major gift candidates.

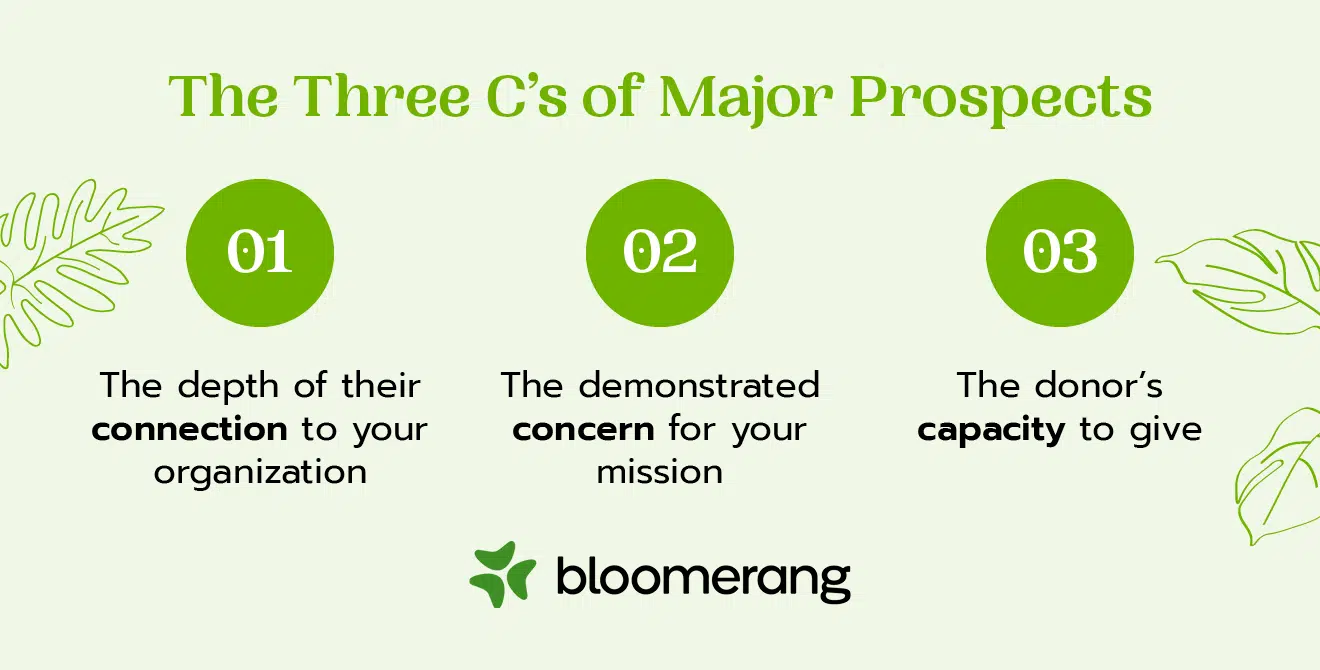

When you start searching your preferred donor database for potential major donors, you’ll want to look at the three C’s of major prospects: the depth of their connection to your nonprofit, the concern they have demonstrated for your mission, and their capacity to give.

Let’s review some specific identification factors to look for in a compelling prospect. In order of importance, these include:

Once you’ve identified these prospects in your donor database, move them through your major gifts pipeline. If you find yourself with too many prospects and limited staff members to build relationships with them all, you could organize prospects into tiers based on each prospect’s overall likelihood to become a major donor to make prioritizing donors easier.

On the other hand, if you don’t have a lot of prospects, strategize how to find more options both within and outside your existing records. As you expand your major prospect list, ask your current major donors if they have any referrals. This not only helps grow your list of prospective donors but also shows the strength of your relationship with the referring donor.

While you care about every donor, you probably don’t have the resources to reach out to all of them individually in the hopes of earning a major gift. That’s why it’s important to follow advice like the Pareto principle, which advises putting 80% of your resources into cultivating the top 20% of prospective donors who are likely to give you 80% of your funding.

When you first reach out to supporters and donors, ask them if they want to build a deeper relationship with your organization. Donors who say they do want a deeper relationship will be possible prospects. Then, consider other qualifications such as if they’ve made past donations that are larger than your average gift amount, if a major donor or board member referred them to your organization, or if they’ve otherwise demonstrated a passion for your mission.

If you’re looking inside your donor database for major donor prospects, take the following steps to understand which supporters to prioritize in your outreach efforts:

While you’re most likely to find your major prospects within your database, don’t discount new supporters’ potential to become major donors. If you need to acquire new supporters and prospects, sit down with board members and stakeholders to see if they have any new donor referrals.

The qualification process is all about getting to know your prospects and building a deeper relationship with them.

In the for-profit world, it takes an average of eight touchpoints with a person to make a sale. In the nonprofit world, we can expect something similar, which is why we recommend trying to reach out to a potential donor eight times to get a conversation. If you make an effort, reach out eight times, and your prospect doesn’t respond, move on to other donors who might.

These eight steps might look like this:

You likely don’t have the time or energy to chase every one of your major prospects. Qualifying them is a great way to make sure they’re interested in maintaining a relationship with you and your organization before you launch into the rest of the gift cultivation process.

Start the cultivation process by developing a concrete case for support that you can share with donors. Keep in mind that donors give because they’re passionate about your mission. In fact, 42% of donors said that hearing personal stories from a nonprofit’s beneficiaries impacted their decision to give. Explaining why you need their support and how they’ll make an impact is key for obtaining gifts.

Start by creating opportunities that allow you to get to know your supporters on an intimate level. For instance, you might decide to create opportunities such as:

As you use these opportunities to build major donor relationships, you’ll want to gather some specific information about them, including:

Track each interaction you have with your supporters and prospects in your CRM to understand how far along in the cultivation process each prospect is and how the relationship is evolving.

So, you’ve started building relationships and cultivating prospects. Cultivate by definition means that you’re leading up to something—and that something is a solicitation. In this case, you’re leading up to making the ask for a major contribution.

There are two primary parts of a solicitation to keep in mind: the meeting setting and the language you use to ask for a donation.

When scheduling a meeting with donors, ask if they prefer to meet virtually or in person.

Virtual meetings are convenient for many individuals with tight schedules and allow organizations to reach donors who don’t live nearby. However, they generally don’t allow for the same level of personal interaction as the in-person alternative.

When you schedule meetings with prospective major donors, make sure to choose an environment set up for intimate conversation. It’s ideal for these meetings to occur in quiet spaces such as a home or office rather than a public setting, allowing for additional privacy and fewer distractions for both parties.

Generally, it’s best to limit the number of attendees. You don’t want your prospects to feel as though they’re being ganged up on by your team. Your executive director, major gift officer, or another team member with whom they’ve developed a relationship are the best choices for the meeting’s importance and personal nature.

If you feel uncomfortable asking prospects for major donations, you’re not alone. We often hear from fundraisers that they feel awkward making such an ask. The good news is that you’re reaching out to people you’ve researched and who you’ve determined are interested in helping your mission. Take comfort in the fact that you’re making an informed ask.

When it comes to making your ask, the first step is to show appreciation for the prospect’s past contributions. As mentioned, it’s unlikely that this person is brand new to your organization and your mission. They’ve gotten involved in several other ways, whether through donations, volunteer work, or event attendance. Tell them about the impact they’ve made and how much you appreciate their support.

Then, when you make the ask, frame it as something for them to consider and provide a specific amount. You should also include the specific program that would benefit from the gift. For instance, you might say something like: “Would you consider contributing a gift of $5,000 for the Save Our Farm program?”

In the best-case scenario, they agree right away. However, you should go into the meeting prepared for them to say no, whether that’s because they don’t have those funds on hand or because they’re not interested in contributing more at this time. If your prospect says no, decide whether it’s appropriate to ask for a smaller gift at that time or if you should just resolve to make another ask in the future.

After you solicit and secure a major gift, you need to follow up and thank your donor for their generosity. Stewardship starts with two simple words: thank you. Show your appreciation for everything your major donors do for your organization and give concrete examples of how you used their donations to help you achieve your mission. This helps cement the relationship you’ve built with them and encourages future involvement with your organization.

Here are a few things you can do to thank your major donors:

Ideally, you will use several of these strategies to show appreciation. If you successfully steward your donors, you’ll likely receive additional financial support from them in the future.

Assess your major giving program results to determine how well the program works and identify opportunities for improvement. Use your CRM to develop a report template to measure your program’s impact.

This report should list metrics such as:

By reviewing these metrics, you can identify opportunities to continue improving your major gift program. For example, if your retention rate for your major gift program is low, you might consider revamping your major donor stewardship and appreciation program.

You should also see specific trends in these numbers over time. For instance, your average donation size and giving capacity will likely increase as your nonprofit grows. If it doesn’t, then consider conducting additional prospect research or increasing your ask amounts.

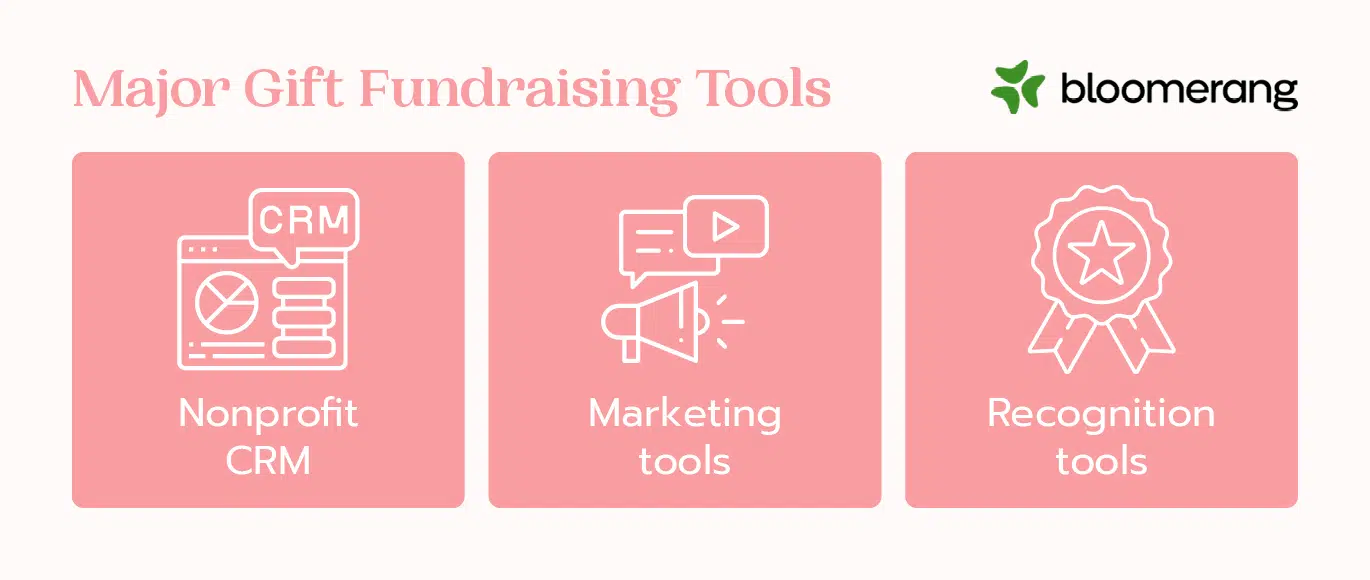

You can leverage several tools to support your major gift fundraising efforts. Here are three of the most helpful options:

Your CRM is your nonprofit’s hub for supporter data. It lets you keep donor touchpoints organized and maintain consistency in your relationship-building efforts. Use your CRM to:

Look for a platform that helps automate many steps of the major donor cultivation and stewardship process. For example, Bloomerang’s donor management system offers built-in wealth screening tools through a DonorSearch partnership, an engagement meter to identify donors most likely to give, and user-friendly filtering and segmentation tools to develop targeted major donor groups.

Marketing platforms help keep your outreach activities consistent and organized. These solutions include email marketing platforms, social media scheduling tools, and direct mail platforms. Your marketing tools can support your major gift strategy by allowing you to:

Recognition tools can support your gratitude strategy by making it easier to thank donors using a variety of outreach methods. For example, you might invest in recognition platforms such as:

Donors will appreciate unique gratitude touchpoints that feel genuine and personal.

A strong major giving program will serve your nonprofit for years to come. Taking the time now to build relationships with major donors will be worth it in the long run when you retain their support and encourage them to spread the word about your organization, bringing new supporters on board.

Want to learn more about how Bloomerang can support your major donor cultivation efforts? Watch this short video and contact our team today to chat about your goals.

If you’re looking for additional support for soliciting major gifts, check out these resources:

Comments