ARTICLE

Strategies to Leverage Donor Advised Fund Philanthropy - FAQs

The use of Donor Advised Funds as a means for individuals to make philanthropic gifts continues to rise and grants from DAFs are becoming a growing source of contribution income for charities of all sizes and shapes. An ever-broader group of Americans are embracing them to approach philanthropy in the thoughtful, strategic way once reserved only for mega-donors who could afford to set up private foundations. These are answers to frequently asked questions about donor-advised funds and should help you understand (1) how they work, and (2)how they may be of benefit to your charity.*

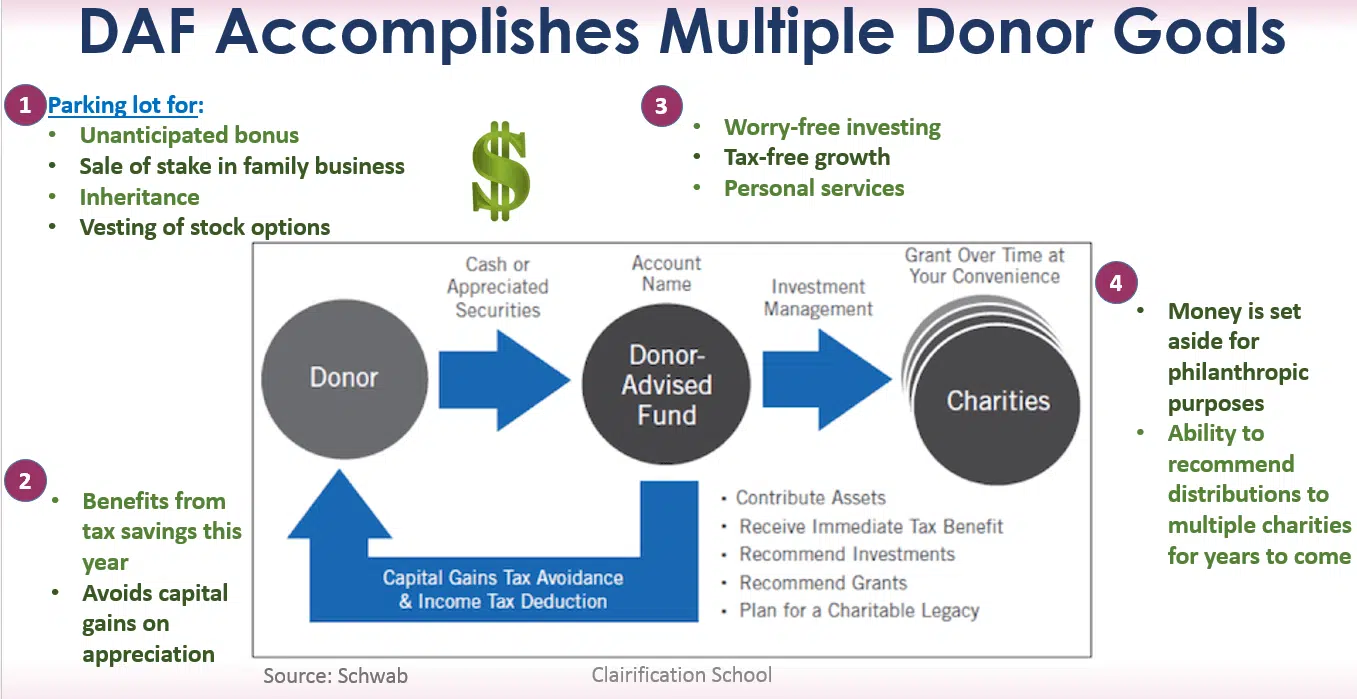

It’s more or less a personal charitable savings account established by a donor with the sole purpose of supporting charities. It is administered by a charitable sponsor organization that has legal control over the donor-advised fund and is responsible for operating and maintaining it. Charitable sponsors include public charities, community foundations, and charitable funds associated with an investment firm. The donor has (1) made the decision to be philanthropic; (2) has not yet decided which charity will be the recipient of their largesse. The DAF acts as a sort of parking lot.

There are four principal reasons:

1. They have a windfall this year, but it’s more than they want to give to any single charity right now. They do want to set it aside for charity, however. By ‘parking’ it in a DAF they get their charitable deduction this year and can recommend distributions from their Fund this year and into the future.

2. They need an income or capital gains tax deduction this year. Regarding income tax, since the passage of the new Tax Act in 2017 fewer donors can itemize deductions unless they reach an amount exceeding the standard deduction. With a windfall (bonus; inheritance; sale of stake in family business; lottery winnings; vesting of stock options) this amount can easily be exceeded. A current DAF strategy is to ‘bunch’ annual charitable deductions by making a gift exceeding the standard deduction to a DAF in one year; then recommending grants over ensuing years when they may make no charitable gifts and simply take the standard deduction. Regarding capital gains tax, if the donor has an appreciated asset, and wants the full benefit of the asset’s fair market value (FMV) when making a charitable gift, they’ll need to donate the asset directly. Were they to sell the asset to get cash for their gift, they’d have to pay capital gains tax on the full amount of the appreciation – thereby diminishing the amount available for philanthropy. Your charity may not accept non-cash assets, while all donor-advised funds accept stock gifts, most will accept a range of personal and real property, and some accept cryptocurrency.

3. They want professional investment and advisory services. Many donors enjoy the freedom that comes from parking their philanthropic money somewhere they won’t have to make investment decisions. There’s a benefit in having their money pooled with other DAF investors, and the money grows tax-free because it’s all eventually going to a charitable purpose. This gives them a growing pot of money to grant to charity. DAF administrators also provide useful services:

4. They like the convenience of a centralized, evergreen philanthropic account. Besides the administrative services offered, donors appreciate being able to recommend distributions for as many years moving forward as they wish (until their death or the death of named successors).

Individuals, families, companies, foundations, and other entities can start a donor-advised fund account.

There’s a low barrier to entry. Donor-advised funds are easy to establish and donors need not go through the time/expense of setting up a foundation, which tend to (1) require larger investments; (2) have more costly start-up and maintenance costs, and (3) allow a deduction only up to 30% of the donor’s AGI, compared with 60% of AGI for gifts to a ‘public charity’ (which a DAF is).

To start a donor-advised fund account generally a minimum of $5K is required; subsequent donations may be smaller. Funds usually set a minimum gift amount, which may be as low as $50. With some administrators, you will need to make an initial contribution of $25,000 or more. Once your account is established, you can make subsequent contributions of smaller amounts.

This varies by sponsoring organization. I’ve made you a little chart that shows investment amounts at a number of DAF sponsors as of this writing:

|

SPONSOR |

INITIAL |

SUBSEQUENT |

| National Philanthropic Trust |

$25,000 |

$5,000 ($1,000 credit card) |

| Vanguard Charitable |

$25,000 |

$5,000 |

| U.S. Charitable Gift Trust |

$10,000 |

$1,000 |

| Fidelity Charitable |

$5,000 |

No minimum |

| Schwab Charitable |

$5,000 |

$500 |

| Silicon Valley Charitable |

$ 5,000 |

Minimum $1,000 balance |

Fees vary by institution. Typically the amount will be based on the balance in the account and/or the number of annual transactions. It is usually under 1%.

This varies by sponsoring organization. I’ve made you a little chart that shows minimum recommended gift amounts at a number of DAF sponsors as of this writing:

|

SPONSOR |

MINIMUM GIFT |

| National Philanthropic Trust |

$250 |

| Vanguard Charitable |

$500 |

| U.S. Charitable Gift Trust |

$100 |

| Fidelity Charitable |

$50 |

| Schwab Charitable |

$50 |

| Silicon Valley Charitable |

$200 ($1,000 outside U.S.) |

Yes. Donors can choose any name for their DAF. They can even call it a Foundation. Most donors choose a name that reflects the main purpose of the account such as “The Clairification Scholarship Fund.” Some donors select a name that helps them remain anonymous, like the “Young Scholars Fund.” Others may name a fund in honor or memory of a loved one, such as “The Lee Axelrad Memorial Fund.”

The sponsoring organization. Once a donor cedes control of the asset, for which they are entitled to a tax deduction, the gift is irrevocable. They cannot get it back. What they can do is make a recommendation as to how the money should be allocated to other charities. The sponsor isn’t legally required to follow that advice; in practice, most sponsors will abide by donor wishes as long as the recommended beneficiary is a qualifying tax-exempt organization and there are no red flags such as pending lawsuits against that charity.

Gifts made to donor-advised funds are irrevocable. Of course, a donor may recommend grants totaling the full amount of their DAF gift(s) and ask the sponsoring organization to close the fund with that sponsor. Sometimes donors will do this if they’re unhappy with fees or services at one sponsor and would prefer to move to another.

Most DAF donors are not the same as the stereotypical foundation donor who establishes a multi-million dollar repository for philanthropy. In fact, because they’re easy to establish, have low overhead, and currently have no strict distribution requirements, a broad spectrum of donors participate. Common characteristics of DAF donors include:

Yes. Depending on the rules of the DAF administrator, most donor-advised funds allow you to choose at least one successor generation. Sometimes successors share advising responsibilities, and can also name their own successor advisors. This option offers the potential for a DAF to exist in perpetuity. Regardless, it never hurts to reach out to donors’ families with a condolence note (not an ask) when you learn about a donor’s passing. It’s a human thing to do, and may inspire the family to make a gift in memory of their loved one.

It depends on the rules of the DAF administrator. If there are no successor advisors, usually donors can designate one or more charitable organizations as account beneficiaries. The DAF sponsor may have a rule allowing the donor to distribute, say, 5% of the account’s balance to the charities that had previously received grants. If a donor had not recommended grants, the entire balance would be transferred to the particular ‘Giving Fund’ or whatever the administrator calls their program. In this case there is generally an advisory panel convened by the DAF sponsor that will pick charities for distributions.

Yes, donors can designate an existing DAF as a primary or contingent IRA beneficiary. This is done simply by writing the name of the DAF, along with the account number, in the Name or Organization Name of their IRA’s ‘Update Beneficiary Designation’ form. Where donors are asked to indicate the beneficiary’s ‘relationship’ to them, they simply say: “My XYZ Donor Advised Fund.” People can even establish a ‘Testamentary DAF’ they plan to fund with proceeds from their estate. When they fill out the paperwork to establish this fund, they simply indicate they want it to be ‘testamentary.’ This lets the custodian know they aren’t funding it yet, but intend to do so at a future date. The donor then receives account information and can use this account name and number when indicating who they want to be the beneficiary of their retirement account. Donors then can enter the names and information of the charities they want to support as beneficiaries of the fund and the percentage each should receive of the total account value once the account is funded. Donors can optionally designate contingent directors who decide which charities to recommend for DAF distributions. It’s a way they might honor loved ones without leaving them a personal bequest. As you may be aware, leaving a traditional IRA to charity is a savvy strategy, as otherwise, these assets can be double-taxed – income taxes never paid during the donor’s lifetime and estate taxes – thereby diminishing the amount received by an individual beneficiary.

No. As you may be aware, donors older than 70 1/2 with traditional or inherited IRAS (not Roth IRAs which have already been taxed) must take required minimum distributions (this requirement was waived for 2020 due to the COVID-19 pandemic) and pay income taxes on this amount. Since 2015 the IRS has allowed donors to transfer the amount of their RMD – up to $100,000 (in 2020 it’s unlimited) directly to a qualified charity. This is known as a “qualified charitable distribution (QCD). The sticking point with donor-advised funds is donors cannot receive any benefit for making a QCD. Since donors retain the right to recommend distributions of the money in their DAF, this is considered a benefit. At least as of this writing. However, donors can name a DAF account as an IRA beneficiary as part of their estate planning.

As noted above, donor-advised funds can be used to leave bequests through a testamentary, financial or insurance vehicle. They cannot be used to fund a split-interest gift (such as a charitable remainder trust or gift annuity) where the donor shares in the benefit through income distributions. Since the gift to the DAF has already received a full tax deduction, the donor is not entitled to additional benefit from this gift. Donors can, however, couple a DAF with a charitable trust in three other ways. (1) They can name a DAF to be the beneficiary of their charitable trust. This way the donor need not decide in advance which specific charity will be the ultimate recipient of their planned giving, and they can have their successors named in the DAF agreement continue to be involved in their charitable legacy. (2) They can fund a DAF through annual income distributions from their charitable trust. (3) They can accelerate their charitable remainder trust, cash out their income interest, and collapse the CRT entirely into a DAF. They will get an offsetting income tax deduction for the value of their income interest.

Since the DAF donor has already received a tax deduction they cannot receive anything of value in exchange for their gift. This means they cannot use a recommended distribution from their DAF to purchase a gala ticket, raffle ticket or auction item. Note that the IRS used to allow ‘bifurcated’ payments where the donor subtracted the FMV of their ‘purchase + donation’ and recommended a DAF gift for deductible part. They then wrote a separate check for the non-deductible part. No more. Section 3 of IRS Notice 2017-73 addresses bifurcated gifts (see below). Internal Revenue Code Section 4967 prohibits DAF grants from conferring any benefits that are “more than incidental” to the donor, donor advisor or anyone related to either of them. Mere attendance – even the right to attend — is considered more than ‘incidental value.’ So you simply must tell your donors they cannot use their donor-advised funds for this purpose. If they do, this can result in the assessment of a penalty excise tax of 125% of the grant on any donor/advisor who recommended the grant or who received the benefit.

The Treasury Department and the IRS currently agree that the relief of the Donor/Advisor’s obligation to pay the full price of a ticket to a charity-sponsored event can be considered a direct benefit to the Donor/Advisor that is more than incidental. Therefore, proposed regulations under § 4967 would, if finalized, provide, that a distribution from a DAF pursuant to the advice of a Donor/Advisor that subsidizes the Donor/Advisor’s attendance or participation in a charity-sponsored event confers on the Donor/Advisor a more than incidental benefit under § 4967. The Treasury Department and the IRS do not currently agree that, for purposes of § 4967, a distribution made by a sponsoring organization from a DAF to a charity upon advice of a Donor/Advisor should be analyzed the same as a hypothetical, direct contribution by the Donor/Advisor to the charity. A Donor/Advisor who wishes to receive goods or services (such as tickets to an event) offered by a charity in exchange for a contribution of a specified amount can make the contribution directly, without the involvement of a DAF.

Suggest to whoever is concerned about angering the donor today that the donor may become a lot angrier tomorrow when the IRS disallows their deduction and imposes a penalty excise tax on them. Tell them you didn’t write the laws and are merely following IRS guidelines – for their and the charity’s protection.

A donor cannot use money for which they’ve already received a 100% tax deduction (i.e., a gift to a donor-advised fund) to pay for something of value to them. Auction items fall into this category unless they are purely for “fund-a-need” items that return no material benefit to the donor. So, yes, you need to let the donor know the gift from the DAF they’ve sent cannot be applied toward their auction item. You can either offer to return it or ask them to send a separate check for the auction item if they still want it.

No. This would be considered a benefit. It’s a quid pro quo exchange – money for advertising.

I’ll give you the by-the-book answer: DAF distributions cannot be used to cover transactions that confer ‘incidental benefits’ on the donor. The same logic and penalty that apply to gifts to cover Gala tickets also apply to membership fees that have deductible and non-deductible portions. See Section 3 of IRS Notice 2017-73.

The Treasury Department and the IRS recognize that a similar issue arises if a sponsoring organization makes a distribution from a DAF to a charity to pay, on behalf of a Donor/Advisor, the deductible portion of a membership fee charged by the charity, and the Donor/Advisor separately pays the nondeductible portion of the membership fee. Therefore, The Treasury Department and the IRS anticipate that the same analysis would apply to a case where the Donor/Advisor receives these types of membership benefits, so that the sponsoring organization cannot pay the deductible portion of the membership fee without conferring more than an incidental benefit on the Donor/Advisor.

It’s a bit murky. The IRS seems to be stricter in its definition of incidental benefits when it comes to gifts made from donor-advised funds (see above) than to gifts made directly to the charity. For the latter, IRS Publication 1771 notes:

Good and services are considered to be insubstantial if the payment occurs in the context of a fund-raising campaign in which a charitable organization informs the donor of the amount of the contribution that is a deductible contribution, and: 1. the fair market value of the benefits received does not exceed the lesser of 2 percent of the payment or $106,* or 2. the payment is at least $53,* the only items provided bear the organization’s name or logo (for example, calendars, mug or posters), and the cost of these items is within the limit for “low-cost articles,” which is $10.60.*

*The dollar amounts are for 2016. Guideline amounts are adjusted for inflation. See IRS.gov for annual inflation adjustment information.

So, you might be safe if the value of the benefits you confer on members in your membership group are less than the guideline amounts. But just the ‘incidental benefit of being included’ in your club or gift society – and any status or special treatment that may accrue — may make payment of any part of this membership not okay. In other words, it’s similar to have the ‘right’ to attend a Gala or other fundraising event, even though the donor might ultimately choose not to attend. In general, the IRS has suggested the following for gifts from donor-advised funds:

Examples of Non-Incidental Benefits (Not OK)

Examples of Incidental Benefits (Generally OK)

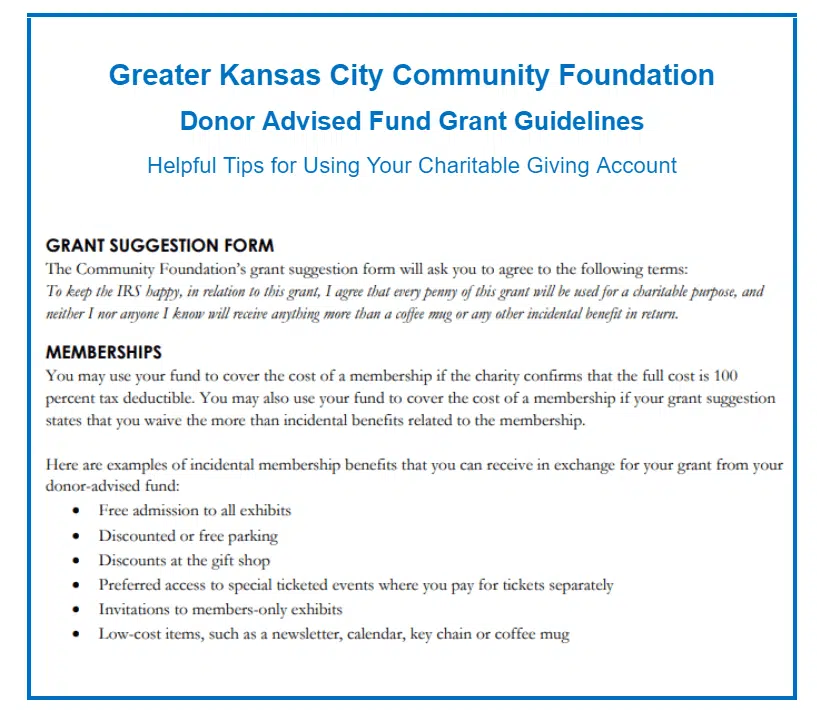

If the donor doesn’t care about the benefits, it’s safest to have them waive more than incidental benefits and to send them an acknowledgment thanking them for their $1,500 gift rather than one welcoming them into your ‘Partners for Life’ society. Note that if an organization has a membership group where they can confirm the gift to become a member is 100% tax-deductible, then this gift would be allowed (this is commonly the case, for example, for museum memberships or dues to religious institutions).

Here is language suggested by one DAF sponsor, the Greater Kansas City Community Foundation, in this regard:

No, and yes. It’s a gray area. Technically, once the donor has made the gift and received the full benefit of the tax deduction, the donor no longer has ownership or control over the money. They are allowed to make recommendations; there is no legal requirement the DAF holder follow these recommendations. Traditionally pledge fulfillment via a DAF distribution was a complete ‘no-no.’ Recently Section 4 of IRS Notice 2017-73 addressed personal pledges, effectively allowing donor-advised funds to make grants that satisfy pledges so long as the DAF sponsor does not reference the pledge in the grant letter or check. The reason for this change was that “allowing satisfaction of Donor/Advisors’ charitable pledges facilitates the giving process.” Even though this is a ‘notice’ and not a ‘regulation,’ you can rely on its advice for now. I still recommend erring on the side of caution. Absolutely do not ask a DAF sponsor to send you a letter indicating the gift is intended as pledge fulfillment! Whether the gift fulfills a donor’s commitment is left to you, the charity, and is not considered the business of the DAF sponsor. I would also recommend against sending a thank you to your donor that references their fulfillment of their ‘pledge.’ You can minimize the likelihood of getting your charity or donor into hot water if you never use the word “pledge” and simply substitute “intent to give.” The former is generally legally binding; the latter is not. This is good practice for all your fundraising, not simply gifts from donor-advised funds. ‘Pledges’ must be booked by your accounting office; ‘intent to give’ commitments need not be booked. If a DAF grant gets your donor ‘off the hook’ for a legally enforceable pledge, the IRS may consider this more than an incidental benefit.

I use this question as a guideline for the treatment of gifts as pledges: Would you be willing to see this headline in your local newspaper — “XYZ Charity Sues Donor for Philanthropic Pledge Fulfillment.” If you wouldn’t go to the mat in this way due to all the negative publicity that would accrue, don’t call it a ‘pledge.’ If the gift is for a capital campaign, and maybe it’s even a lead gift upon which your campaign substantially relies, then you might think about this differently. In which case you’d ask the donor to sign a legally binding pledge agreement. In the case of a legally binding pledge, the donor could not fulfill it with a gift from a DAF.

Donors who give to any qualified 501 (c) (3) charity – of which DAFs are included – may deduct up to 60% of their adjusted gross income (AGI). When they give to a private foundation they can only deduct up to 30% of AGI. This is one of the features of a DAF that makes them popular. You may be aware the 60% limit has been lifted in 2020 to 100% (by the CARES Act), but that applies only for cash gifts. And this increased cap does not apply to gifts to donor-advised funds as I understand the law. See also: How to Let Donors Know New CARES Act Offers Deduction Opportunities.

When donors set up a DAF with a community foundation or any other sponsor they are giving to a spin-off 501 (c) (3) created by the sponsor. So the percentage limitation for deductions is higher than a straight gift to the foundation.

It varies. Many nonprofits report DAF donors make average gifts that are larger than non-DAF donors. This is something you can calculate for your own nonprofit. Per Vanguard Charitable their average DAF gift is nearly $12,000. Yet such averages are heavily skewed by donors with large fund balances. Fidelity Charitable reports more than half of its donors have balances of less than $20,000, so thousands of smaller gifts are made. You can find comprehensive annual reporting on DAF contributions, grants, and account balances compiled by National Philanthropic Trust.

This question is mixing apples and oranges. Foundations have a 5% minimum payout requirement and often do not exceed this. DAFs generally have no payout requirement (though individual sponsoring organizations may set a minimum) and often give out more than 5%. A DAF is not an endowment fund, which is generally designed to keep the principle intact and spend the income. Donors may recommend out the full amount in their DAF every year, as long as they keep whatever balance is required by the sponsoring organization (often as little as $1,000).

Generally, no. The reason is if someone other than the donor or someone they’ve specifically authorized to make gifts and/or distribution recommendations as advisors or successor advisors (e.g. family members; partners) gives to the DAF, this individual will get an immediate tax deduction. Yet they’ll simultaneously be receiving a value in return (the value of gifting money for charitable distribution to their honoree). Since donors cannot receive something of value in return for their tax-deductible contribution, this is not allowed.

No good reason! What you really want to do is get inside the donor mindset. People have funny way of making assumptions. If you don’t let them know you accept gifts from DAFS or, for that matter, gifts from IRAS or bequests from wills or trusts, folks just won’t think of you when it comes to making these types of philanthropic distributions. For donors who’ve already set up a DAF, having this on your website as a giving option simply serves as a reminder to them that they have a philanthropic pot of money awaiting distribution. If you make it easy for them to give to you from this pot, they may just do so. If you don’t make it easy, they’re less likely to consider this method of giving to you.

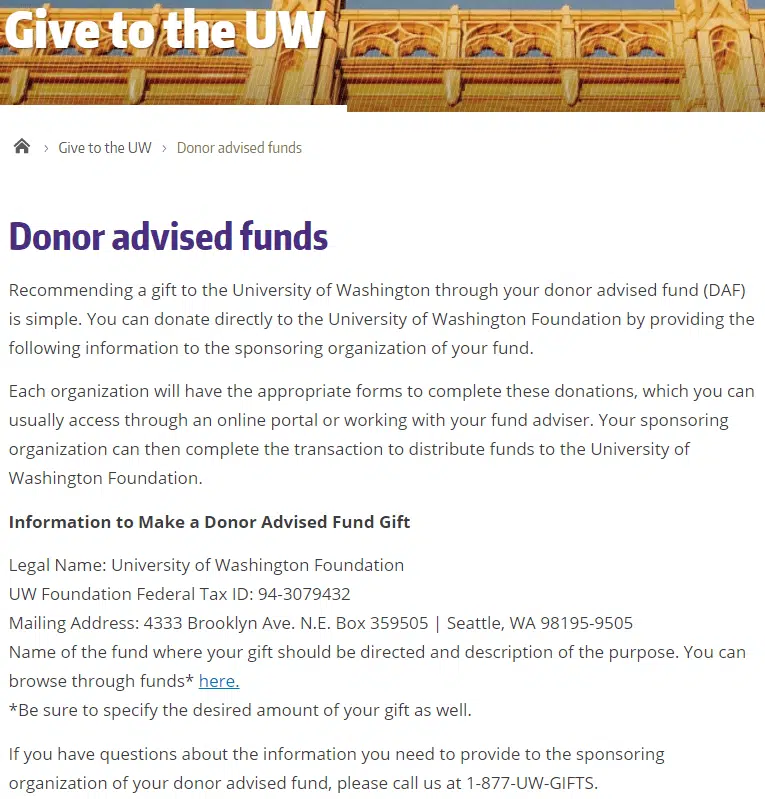

The best, and easiest, solution is simply to include giving from DAFs as a drop-down option from your ‘donate’ or ‘ways to give menu.’ Here are some examples from the International Rescue Committee, Jewish Family and Children’s Services, and University of Washington:

Another strategy is to include testimonials on these pages from other DAF donors to your organization. This acts as ‘social proof’ your organization is ‘DAF-worthy,’ and may inspire copycat donations. I’ve often had donors call me to say “If Vera and Hal can do that, so can we!” Here is a testimonial example from Jewish Family and Children’s Services:

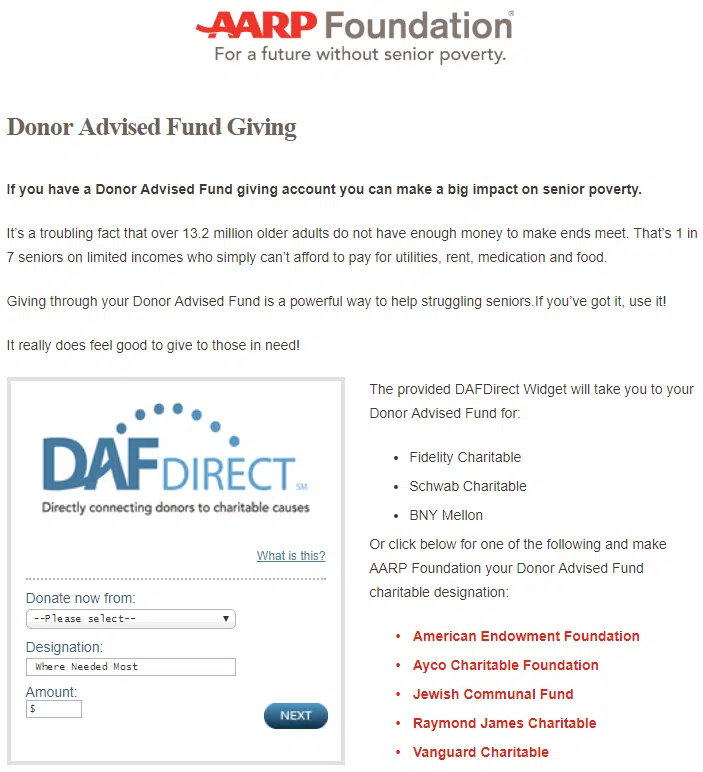

To make giving easy, consider including a widget that enables transfers from DAFs at selected administrators to your charity. I’m most familiar with the DAF Direct widget, which is free. Check it out here. They include a list of nonprofits using the widget, so you can see how other organizations incorporate it into their websites. I’d say its chief limitation is that it only includes a handful of DAF repositories. I’m unclear if there is a way to customize the widget to add additional DAF sponsors. But… you can add other options alongside the widget. I’ve noticed charities adding their local community foundation, for example. And you can see other examples below. You might need to pay a contractor to add additional options alongside the widget. Or your own technical staff may be able to accomplish this. For an example, check out the options in red on the AARP website:

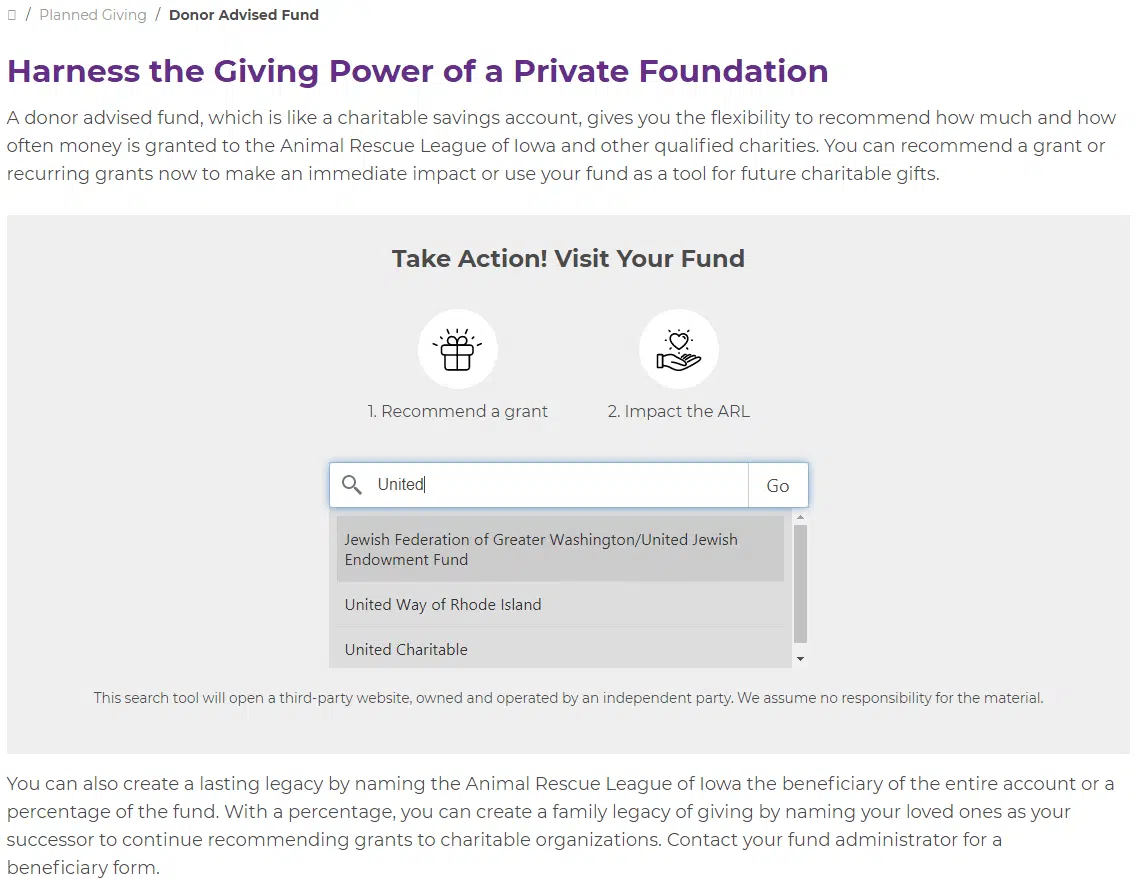

MarketSmart has a widget in Beta. The Stelter Company has a promising widget (free now to their clients; available to all in 2021) that enables would-be donors to type in the name of their DAF sponsor. If it’s in the system, the would-be DAF donor will get a drop-down with a link that will take them directly to their sponsor’s log-in so they can instantly make their recommendation. If their sponsor of preference is not yet included, the donor will get a prompt and Stelter will add the link. Contact them if you’re interested. Here’s one example from Animal Rescue League of Iowa. I typed in the word “United” and you can see the options it gave me:

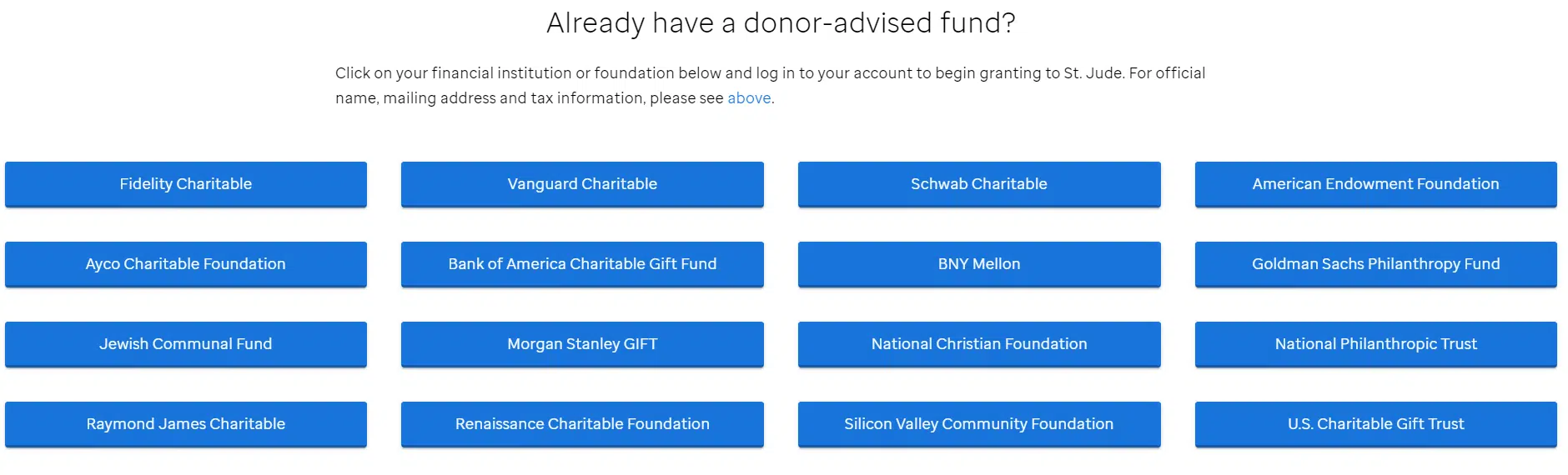

Some organizations who receive (1) significant amounts of DAF recommendations from a wide variety of vendors, or (2) a preponderance of DAF recommendations from DAF administrators not included on currently available widgets, forego the widget entirely and set up their own links to DAF sponsors. See the following example of how St. Jude Children’s Research Hospital does this:

The widgets described above are designed for individual charities so they can make it easy for donors to recommend gifts directly from their DAF. When you put a DAF Direct widget on your website it will generally take donors to a log-in page with the sponsoring entity. Donor-advised fund sponsors, like community foundations, financial institutions, and charities like Jewish federations, tend to have different software to enable donors to make gift recommendations. Take a look at one example from DAF sponsor Jewish Family and Children’s Services.

There are several ways to make a positive impression. The easiest, and probably most overlooked, strategy is to claim your Candid/Guidestar online profile. Many DAF sponsors share this nonprofit profile information with their donors. If they don’t share it, they use it themselves to help their clients make informed, strategic decisions. (E.g., Vanguard Charitable advisors, as they research charities to support, make more than 15,000 searches each month via this National Nonprofit Directory. Even were DAFs not to exist at all, there are tens of millions of donors who search this resource – and you should put your best foot forward. It’s the cheapest advertising around!

Another strategy that works well with local community foundations is simply to reach out to them and ask for a meeting to update them on your work. Often these advisors are looking for organizations (like yours!) to recommend. You provide an invaluable service by offering on-the-ground insight into root causes of problems and opportunities to make a difference. It’s not unusual for those who’ve established a DAF to see an article about something in the newspaper; then ask the foundation advisor with whom they work if any local nonprofits are addressing the issue. Or they may have a particular area of passion and want to know who is doing good work. Get on these advisors’ radar; build a relationship. These folks influence millions of dollars of philanthropy!

Ask them! It’s always a good idea to ask all donors what vehicle they’d like to use to make their gift. This is something you can include as a check-off box on your remit pieces and donation landing pages. If you’re soliciting major donors, this is something you can simply ask them in person: “Do you have a DAF, and might you want to consider recommending a gift here?”

Since passage of the Tax Act of 2017 fewer donors can itemize deductions unless they reach an amount exceeding the standard deduction. Donors can exceed this limit during a year where they have some sort of windfall. This is where they might engage in “bunching,” where they make a gift to their DAF, take a BIG deduction this year, and then make no philanthropic contributions the following year – when they simply take the standard deduction. They are then able to recommend distributions from the “bunched money” in their DAF over ensuing years they don’t make a BIG “bunched” gift. [See Major Donor Fundraising: What to Know about the New Tax Law].

You can turn bunching to your favor! These donors now have a DAF filled with charitable money just waiting to be distributed! When you approach them for a gift this year, they may just have forgotten about this little ‘burning pocket.’ It’s a painless way for them to give, and you may end up with a larger gift than you’d otherwise have received — just because you gave them a reminder!

Of course! This is something you can add to your thank you letters to donors who recommend DAF distributions to your nonprofit. Just a single line can be effective: “Your support means the world, and we’d be honored if you would consider naming XYZ Charity as a recurring and legacy beneficiary of your Fund.” Most sponsoring organizations will facilitate legacy and/or recurring giving on behalf of your donor.

This is a two-part practice:

As with all individual donors you want to engage with DAF donors repeatedly throughout the year to build a relationship that will influence their loyalty. This means whenever you run acknowledgment, recognition, and stewardship reports from your database you want to be sure to add instructions to your query to include soft credits. The same holds true for appeals queries. You’d hate to ask the DAF sponsor for a gift next year and neglect to ask the individual donor! DAF sponsors don’t recommend gifts; individual donors do.

There is no hard and fast rule. What I like to do is to list the donor by their name; then list the sponsoring organization separately – but just one time. For example, if you receive 11 gifts recommended from donor-advised funds established at Vanguard, simply list Vanguard Charitable one time. This means cumulating all the gifts you’ve received from Vanguard Charitable over the course of the year so you recognize them appropriately by giving level. Try to always ask donors how they prefer to be listed. Some may prefer Joe and Mary Goode. Others may prefer The Goode Family Fund.

The most important thing is that you not thank donors for their “tax-deductible” gift or in any way convey information that may confuse a donor or their advisor. Since the gift has already received a full tax deduction, I prefer a thank you letter that says the following:

“Thank you for your $1,500 gift recommended from your Jen Generosity Fund at Vanguard Charitable.”

This reassures the donor you received the full amount they recommended but also alerts them and their accountant the gift is not eligible for a deduction at this point.

I would disagree. DAF donors do benefit from a tax deduction, but this means their gift simply costs them less. They’re still parting with their money. Most people want to see an impact from their gift rather than letting it sit unused. In fact, at last reporting, Schwab Charitable said 80% of its contributions were fully distributed to charity within 10 years. Fidelity said 74% of its contributions were distributed within five years; 84% within 10 years. Sometimes donors just forget the money is there – and that’s where you come in. When you promote DAF giving, you remind donors this option exists. The payout rate from DAFs has actually exceeded 20% every year since 2014. According to National Philanthropic Trust data, most donors are active, making an average of six to seven gift recommendations annually. Even though donor-advised funds may merit reforms that require more to be distributed, these giving vehicles remain an active source of philanthropy of which you should be cognizant.

Some grants from donor-advised funds don’t include the full name and address of the donor. But that doesn’t necessarily mean the donor’s identity is a mystery. In fact, generally, only around 5% of DAF donors choose to remain anonymous. Here are some suggestions for sleuthing out the source of the grant recommendation:

Some DAF sponsors will forward on thank you letters from you to anonymous donors. It’s definitely worth asking them if they will do this on your behalf. It’s more challenging with the large national financial institutions, but I’d definitely recommend trying. You may find a responsive, empathic person answers your call! You’ll definitely have more luck with more local sponsors. At the very least, when you mail your thank you letter to the funder, send them an extra thank you intended for the donor. These advisors are people too, and many understand how much their donors may appreciate receiving an acknowledgment or impact report from you. This is why it’s a great idea to reach out to donor-advised fund professionals at your local community foundation, United Way and/or Jewish Federation. Let them know what you’re up to, as they often monitor their donors’ interests. If they can make a match between one of their DAF donors and your nonprofit it’s a win for everyone.

Of course, you should adhere to expressly stated instructions of the granting organization. If this is where the larger donor-advised funds sponsored by financial institutions are moving, then only thank the individual donor. Yet I imagine it’s NOT the case with DAF gifts coming out of local community foundations, United Ways, Jewish Federations, and gifts from DAFs established at other 501 (c) (3) charities. In those cases, I’d suggest it’s still good practice to send a written thank you to the institution. Better still, try to set up a meeting with whoever is responsible for meeting with DAF donors and talk about ways you can work collaboratively in service to their/your donors. Of course, what’s MOST important is cultivating and stewarding the individual donor. So… double up on that!

I recommend scouring annual reports of local and/or social benefit organizations similar to yours. See if you find any hints. For example, do you see a donor listing for the “Jen Generosity Schwab Fund?” The “Jen G. Fund at the San Francisco Foundation?” Or even simply the “Jen Generosity Fund?” If Jen Generosity is one of your donors, yet you’ve never received a gift from her fund, you might reach out to her to see if she’d like to consider making her next gift to you from that Fund. Or just make a note in her donor record so the next time you chat with her about a gift, and she says she can’t make as big a gift right now as she’d like to, you can ask her if she might have non-cash assets from which she might direct her giving. Do this in a helpful way, of course: “Some of our supporters this year are making gifts from their donor-advised funds since that money is already set aside for charitable giving; might you have an established DAF?”

The large financial institutions do not generally list the names of their donors in their annual reports, but I haven’t searched for all of them. You can find more information by searching their financial reports on Candid/Guidestar. You’ll generally find names of grant recipients, not donors.

Community foundations, United Ways, and Jewish Federations often publish annual reports listing their donor-advised funds. If they don’t list all of them, they may include a sampling of testimonials. You might just get lucky and find someone who would be a good fit for your organization! Here’s a listing with several DAF donor stories from Jewish Family and Children’s Services in San Francisco (where I began their DAF program many moons ago – and it’s going strong!).

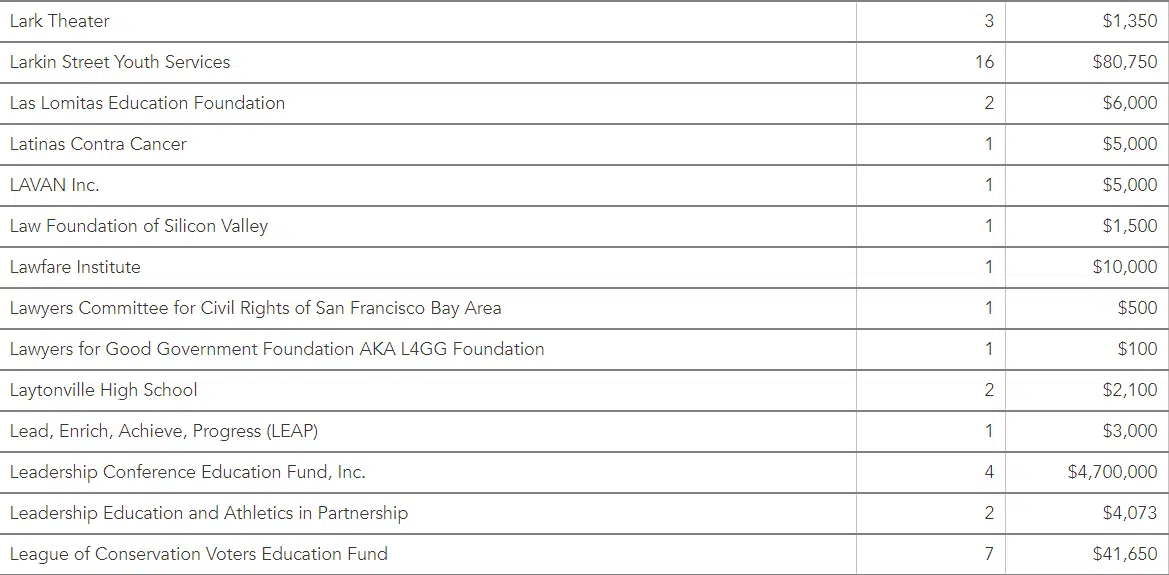

Sometimes you may not be able to find listings of donor names but you can find grantee listings. Here’s an example I found on the website of my local Jewish Community Federation:

This may be interesting to you if you run a youth services program or an environmental program since you can see they’ve had 16 donors make grants to Larkin Street Youth and 7 made grants to the League of Conservation Voters Education Fund. Why not reach out to the Federation and see if you can meet with them to let them know what you’re up to?

Donor-advised funds often accept gifts of assets charities are not equipped to handle. This includes gifts of personal property, real estate, closely-held businesses, and, yes, cryptocurrency. Donating in this manner enables donors to eliminate any capital gains taxes and give the full fair market value to charity. So if a donor wants to give you cryptocurrency, and you don’t accept those types of gifts, you might suggest they consider setting up a DAF; then sending a recommended grant your way.

Yes, if the DAF is one that accepts gifts of real property. Generally, it must be marketable and free of debt. And there can be no pre-arranged sale pending. The donor irrevocably transfers the property; when the property sells, the net proceeds will be used to fund the DAF. Most of the larger sponsoring organizations accept such gifts, but they all have their own rules. If you’re speaking with a donor who is considering establishing a DAF for this purpose, you may want to help them, as a donor service, to research the DAF sponsors that accept such gifts. I don’t recommend you advise them to set up their fund at any one particular organization, but it is fine to give them a couple of leads to pursue on their own.

DAF donors are like any other donor, but perhaps on steroids when it comes to ongoing stewardship. Why? Because they tend to be extremely thoughtful about their philanthropic investments and, therefore, interested in outcomes. They will respond especially well if you send ongoing reports letting them know how their investments are doing.

Whether your donor recommends grants from their DAF of $10,000 or $10 million a year, often they decide based on a larger vision/goal — addressing needs in the local community or making a dent in broader social problems. In fact, the typical Fidelity Giving Account donor has an average portfolio of eight charities. For DAF donors to connect the dots in their giving portfolios wisely, they need feedback from populations they seek to help. This is an opportunity for you to:

*IMPORTANT CAVEAT: These answers are offered based on my understanding, to the best of my knowledge, and are not to be relied upon as professional legal or financial advice. As laws and regulations are always changing, and open to interpretation, you should always consult with your own professional advisors. A review of IRS “do’s and dont’s” will assist with compliance and may save your organization from an expensive and embarrassing violation. See IRS Donor-Advised Funds Guide Sheet Explanation.

I hope you’ll consider enrolling in “Clairification School” to support my efforts to empower small to medium-sized nonprofits who don’t have large budgets for training and consultation. Consider Clairification your online, year-round fundraising school.

I’ll tell you not just what to do, but why. You’ll get tons of useful content — pretty much for peanuts — because I’m dedicated to giving you the knowledge you need to succeed. Some folks have told me it’s “ridiculously inexpensive” for what you get — and I hope you’ll think so too!

My motto is “If I know it, I want you to know it!”

As others taught me, so do I wish to teach you.

Comments

David Gladfelter

Aaron Shaver